RBI flouts its own directive and defies Supreme Court to protect big corporate defaulters, putting the entire banking system at great risk, while crying foul over farmers' loan waivers - paid for by state governments and relatively inconsequential

Prasanna Mohanty Last Updated: November 6, 2019 | 11:17 IST

Prasanna Mohanty Last Updated: November 6, 2019 | 11:17 IST

The RBI's very same September report also points out a large-scale diversion of agri-credits for non-farm use

In August, the multinational banking and financial services company Credit Suisse warned of a "second wave of NPAs" in India with the banking sector's stressed loans likely to exceed 12% as a debt of Rs 2.4 lakh crore across 16 stressed corporates is being put through the inter-creditor agreements (ICAs). The ICAs, notified by the RBI in July this year, is the only restructuring framework now available to banks before the Insolvency and Bankruptcy Code (IBC) kicks in.

A month later, in September, the RBI released 'Report of the Internal Working Group to Review Agriculture Credit', pointing out an "unprecedented increase" in agriculture loan waivers during 2014-2019 by 10 states, totalling Rs 2.4 lakh crore and blaming it for increasing the agriculture NPAs "sharply" to 8.44% in FY19.

The report dismissed farm loan waivers as "not the panacea" and added: "In fact, they destroy the credit culture which may harm the farmers' interest in the medium to long term and also squeeze the fiscal space of governments to increase productive investment in agriculture infrastructure."

Few can argue against this. But before getting into the blame game, here is a reality check.

Reality check: Who is responsible for growing NPAs?

The following two graphs plot the RBI data on sectoral share of NPAs of the scheduled commercial banks (SCBs) - which include public sector banks (PSBs), private and foreign banks providing banking services in India.

They show that the agriculture's share of total NPAs is 8.5%, on an average, in three years between FY16 and FY18 for which data are readily available, as against an average of 76.7% for the "non-priority sector". The non-priority sector entities are the medium and large industries operating in the manufacturing and services sectors.

In absolute numbers, the agriculture NPA for FY18 was Rs 0.83 lakh crore, while that of the non-priority sector was Rs 7.56 lakh crore - 9 times higher.

A 2018 study by the Delhi-based Institute for Studies in Industrial Development (ISID) sheds more light on the sectoral share of NPAs. It says the NPA problem "primarily originates from the non-priority sector loans". These are of "the large corporate industries" which are also "the large borrowers" operating in metal, cement, textile, paper, mining, food processing and construction sectors, rather than agriculture, services or retail sectors.

Most of these NPAs are in the accounts of the PSBs, as the following graph would make it clear.

Farmers' loan account for about 2.4% of total NPAs

The agriculture NPA also includes loans of big farmers and food and agro-processing units, besides the small and marginal farmers who benefit from the loan waivers. What would then be the share of small and marginal farmers?

Here is a back of the envelop calculation.

All loan waivers announced are for a maximum of Rs 2 lakh - except Tamil Nadu which put "no limit" but waived off only those loans from the Rural Co-operative Credit Institutions (RCCI), which are out of the SCBs' ambit. Since loans of up to Rs 2 lakh account for 39% of the total agriculture credit (eight-year average as per the RBI database), the loan waivers could be assumed to be to this extent in the agriculture NPA of 8.5%.

Further, 29% of loan waivers in value (Tamil Nadu, Rajasthan and Karnataka) have no SCB component. Therefore, the loan waiver would be lesser by this extent too. In fact more should be deducted since the rest seven states have non-SCB loans also - loans from the RCCIs, RRBs, DCCBs and other cooperatives.

Once these two factors are taken into consideration, the actual farmers' loan component comes to 2.4% of the total NPAs of the SCBs.

Surely, if a waiver of 2.4% of NPAs could be damaging to the credit culture, fiscal space and investment, then 97.6% of NPAs would be far more devastating - 97.6 times more. That should be making the RBI very worried. But does it?

State governments pay for farm loan waivers

Even this 2.4% of agriculture NPA could be misleading.

The RBI's very same September report also points out a large-scale diversion of agri-credits for non-farm use. It says that in many states the total agri-credit for agriculture has been found to be far more than their agri-GDP (Kerala - over 180%, Tamil Nadu - 170-180%, Telangana and Punjab - over 100%). This is, apparently, because of very low agriculture interest rates.

The RBI has less to complain about farm loan waivers also because the state governments pay for this entirely from their budgets, while banks write off NPAs on their own which is a reflection of their own failures and incompetency which endangers India's economic wellbeing. At times, the central government helps these banks through recapitalisation. Since FY015, the banks have been recapitalised by Rs 3.82 lakh crore.

The moot question then is: Why such a hullabaloo by the RBI against farm loan waivers?

RBI does not disclose the identity of big defaulters

Defying logic, its own guideline and the Supreme Court's repeated warnings and reprimands, the RBI zealously guards the identity of big defaulters year after year.

Shailesh Gandhi, former member (2009-12) of the Central Information Commission (CIC), says he alone had given 10 orders to the RBI during his tenure to disclose the identity of big defaulters, audit and actions taken reports, in response to RTI complaints. The RBI refused to comply on the pleas of economic interest, commercial confidence and fiduciary relationship with other banks.

In December 2015, the Supreme Court (SC) rejected such pleas, upheld the CIC orders and directed the RBI to comply. The RBI defied again, leading to contempt proceedings. In its April 2019 order, the Supreme Court severely reprimanded it for "continuing to violate the directions by this Court" and issued a warning: "Any further violation shall be viewed seriously by this Court."

A fresh RTI application has been filed by one of the litigants in July. The reply is still awaited.

After the PMC bank scam hit, Gandhi wrote about his experiences with the RBI with this observation: "It is essential for the Reserve Bank of India to understand its primary role of service to citizens and to realise that India will benefit if it transparently does its job of regulating financial institutions."

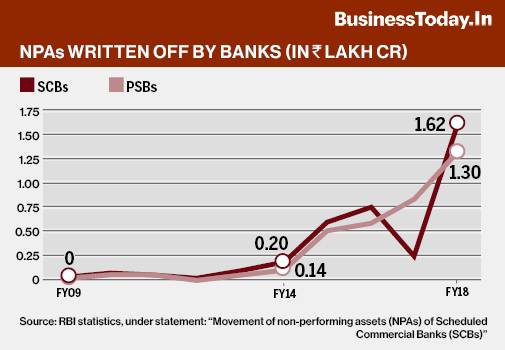

RBI stops disclosing NPA write-offs as well

That is not all. The RBI has stopped disclosing NPAs being written off.

Its database did have such information until August this year (from FY05 to FY18), under the column "write-off during the year", which has now been taken out.

A saved copy of this datasheet in August is plotted in the following graph.

The writing-off shot up from FY09. During the period of FY05 to FY18, the SCBs wrote off Rs 3.84 lakh crore of NPAs - of which Rs 3.6 lakh crore was by the PSBs.

How much was written off in FY19?

The RBI is not revealing. However, prominent national dailies have said their investigations reveal a whopping Rs 2.54 lakh crore was written off in FY19 and that the SBI admitting (in response to RTI) to writing off Rs 76,000 crore of 220 corporate defaulters who owed more than Rs 100 crore each.

RBI flouts its own directive regarding disclosures

Gandhi draws attention to an interesting RBI circular of 1994, which set out a new scheme, "Scheme on collection and dissemination of information regarding defaulters of Rs 1 crore and above". It asked the banks to file regular reports on the defaulters with a view of sharing with other banks and financial institutions (FIs). The objectives were two:

- "alert the banks and financial institutions and put them on guard against borrowers who have defaulted" and

- "publish a list of defaulting borrowers in cases where suits have been filed by banks and FIs", i.e., make the details public.

Had the RBI followed its own scheme or counsel to the banks under its regulatory control, many banks wouldn't have given huge loans to some of the big corporate defaulters, many of whom have now fled the country.

No comments:

Post a Comment